Table of Contents

Introduction

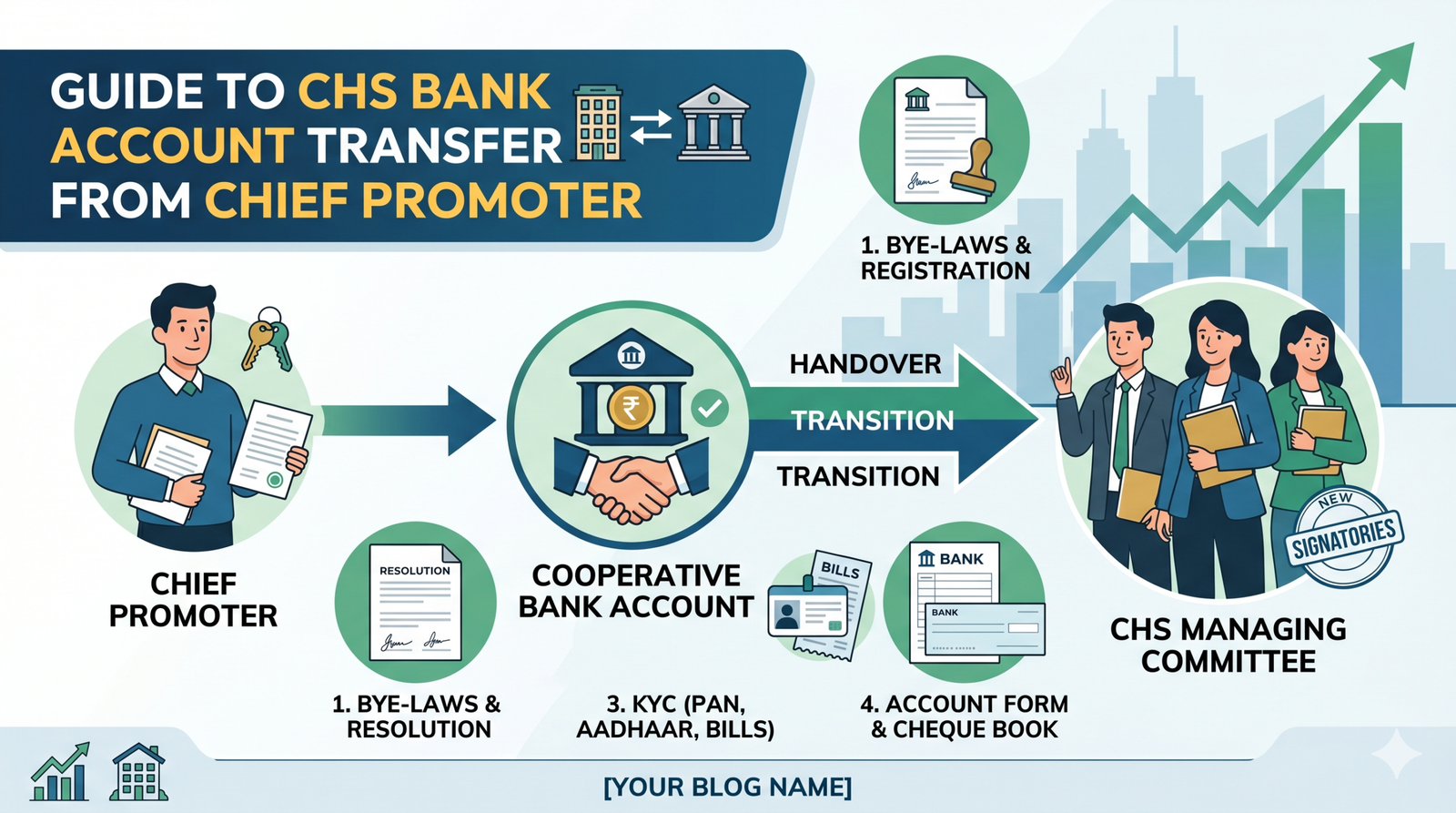

CHS Bank account transfer from Chief Promoter: If you have recently registered a new Co-operative Housing Society (CHS), one of your first financial duties is the CHS bank account transfer from Chief Promoter to Society’s name. Initially, the account is opened by the Chief Promoter (CP) to collect share money and entrance fees. However, once registration is complete, that control must shift to the newly elected Managing Committee.

In this guide, we break down the legal timelines, required documents, and the step-by-step process for a smooth CHS bank account transfer from Chief Promoter.

1. Legal Timelines for the Account Transfer

Under the Maharashtra Co-operative Societies (MCS) Act, the CHS bank account transfer from Chief Promoter is not an open-ended process. It follows a strict schedule:

- First General Body Meeting: This must be conducted within 3 months of the society’s registration date.

- Handover of Funds: The Chief Promoter is legally required to hand over all records and bank balances to the new committee within 15 days of the first meeting.

- Bank Intimation: To ensure financial security, the committee should initiate the CHS bank account transfer from Chief Promoter at the cooperative bank within 7 working days of electing office bearers.

2. Document Checklist for CHS Bank Account Transfer

To successfully process the CHS bank account transfer from Chief Promoter, the Manager of the cooperative bank will require a specific set of documents. Ensure all “True Copies” are signed and stamped with the society seal.

- Society Registration Certificate: A true copy issued by the Registrar.

- Registered Bye-laws: A true copy of the approved society Bye-laws.

- Society PAN Card: A copy of the PAN card issued in the society’s name.

- NoC from Chief Promoter: A formal No-Objection Certificate on plain paper signed by the CP.

- Meeting Resolutions:

- True copy of the resolution from the first General Body Meeting held with the CP.

- A specific Resolution for account transfer and the designated “Mode of Operation” (who will sign cheques).

- KYC of Office Bearers: Self-attested copies of PAN Card, Aadhaar Card, Maintenance Bill, and Electricity Bill for the Chairman, Secretary, and Treasurer.

- Account Opening Form: A fresh form provided by the bank, signed by the new authorized signatories.

3. The Transfer Process: Step-by-Step

Once you have the documents ready, follow these steps to finalize the CHS bank account transfer from Chief Promoter:

- Step 1: Visit the cooperative bank where the CP initially opened the account.

- Step 2: Submit the complete dossier to the Branch Manager.

- Step 3: The bank will update the “Authorized Signatories” in their system.

- Step 4: Collect the new cheque book and updated passbook in the society’s name.

4. Common Pitfalls & How to Avoid Them

Many societies face delays in the CHS bank account transfer from Chief Promoter due to simple errors. Keep these in mind:

- The “Proposed” Name Issue: Sometimes the CP account is in the name of “Proposed [Society Name].” Ensure the new account reflects the exact name on the Registration Certificate.

- Signature Discrepancies: Ensure all committee members sign the bank forms exactly as they appear on their PAN/Aadhaar cards.

- Address Mismatch: If the society’s registered address is different from the physical location (common in new builds), provide the bank with the registration certificate as proof of the official address.

5. Frequently Asked Questions (FAQs)

Q1: Can we keep using the Chief Promoter’s account for a few months?

No. It is legally required to initiate the CHS bank account transfer from Chief Promoter immediately after the first General Body Meeting to avoid mismanagement of funds.

Q2: What if the Chief Promoter is not cooperating?

If the CP refuses to provide the NoC or handover the funds, the Managing Committee can approach the Assistant Registrar of Co-operative Societies to seek an order for the transfer.

Q3: Can we open the account in a Private Bank?

Under Maharashtra law, housing societies are generally encouraged to keep their primary accounts in Cooperative Banks or Nationalized Banks. Check your specific Bye-laws before choosing a private bank.

Disclaimer

Disclaimer: This blog post is for educational purposes only. While I am a professional society manager and insurance advisor, laws under the MCS Act and RBI banking norms are subject to change. Always consult with a legal professional or your local Registrar’s office for specific compliance advice.

Ram Niwas Bansal

“Dedicated and highly qualified professional with a specialized focus on Cooperative Housing Society (CHS) Management and Legal Advocacy. Leveraging a strong technical background and an Indian Air Force veteran’s discipline, I provide end-to-end solutions for housing societies in Mumbai.

With a Government Diploma in Cooperation and Accountancy (GDCA 2024) and a Diploma in Naturopathy, I bridge the gap between administrative excellence and holistic community well-being.