Table of Contents

Introduction

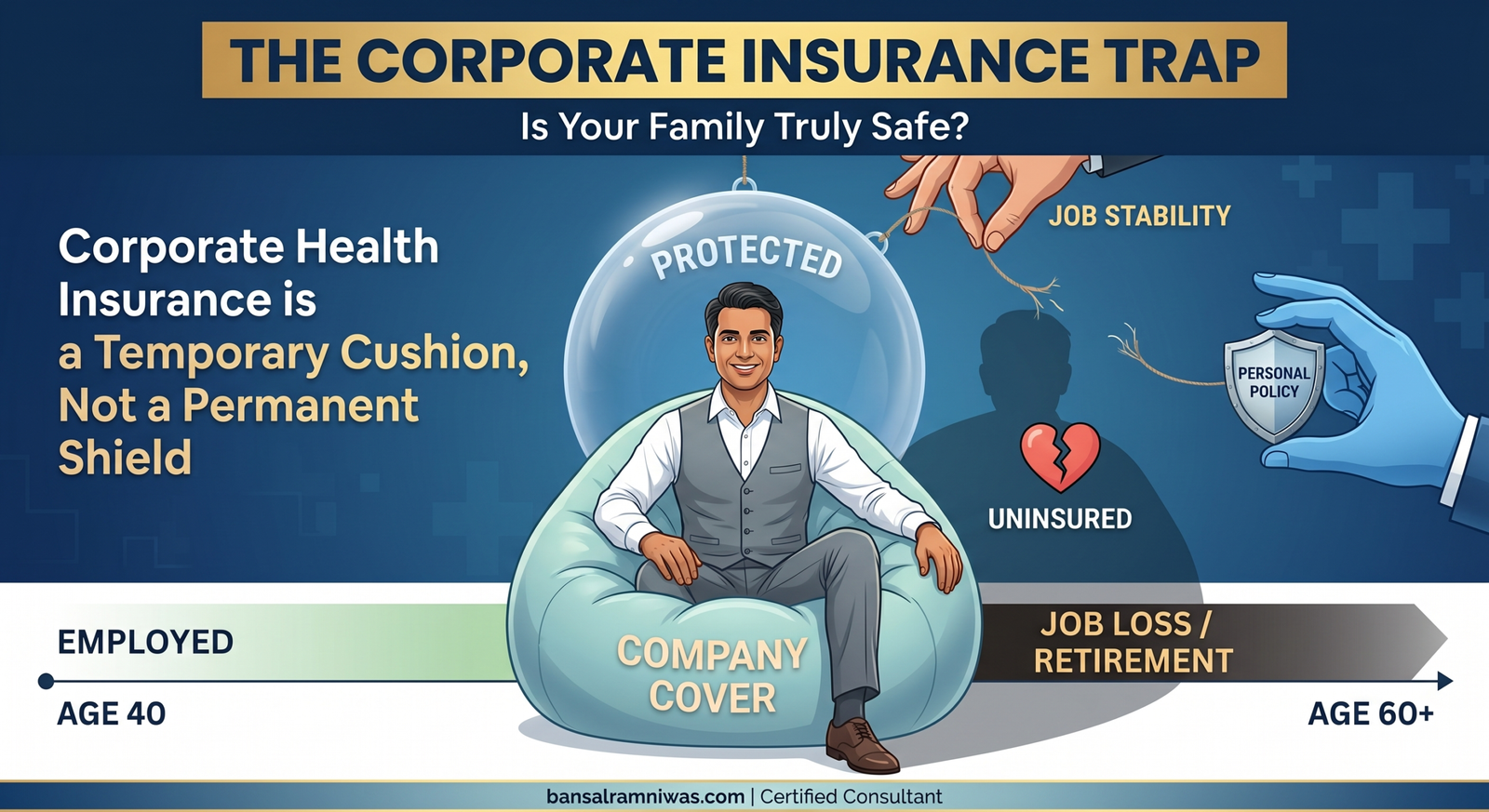

Company Health Insurance vs Personal Policy: If you are a corporate employee who confidently believes: “My company covers me and my family with a 5 or 10 Lakh health insurance policy, so why do I need a personal one?” …you might be making the biggest financial mistake of your life.

Holding that company health card feels incredibly reassuring. But the harsh reality is that you are driving a beautiful car where the control of the brakes belongs to your boss. The exact moment you leave the company or retire, those brakes vanish.

Let’s look at the 5 hidden risks of relying solely on employer-provided health insurance—risks that your HR team will never tell you about:

1. The “Waiting Period” Trap ⏳

Company Health Insurance vs Personal Policy: The biggest misconception among employees is: “I will simply buy a personal policy the day I quit or lose my job.” Even if you are perfectly healthy and successfully get a new policy the very next day, the strict rules of insurance do not change:

- The Initial 30 Days: Absolutely no coverage for any illness (only accidental hospitalizations are covered). If you contract dengue, malaria, or suffer a medical emergency on day 15 after leaving your job, you pay 100% out of pocket.

- The 2-Year Specific Illness Wait: Insurance companies have a mandatory list of common ailments—like cataracts, kidney stones, hernia, and joint replacements—that are strictly locked out for the first 24 months of any fresh policy, regardless of your current health status.

- Pre-Existing Diseases (PED) Wait: If you already have lifestyle conditions like diabetes or hypertension, a fresh policy will make you wait 3 to 4 years before paying a single rupee for treatments related to them.

The Early Advantage: If you buy a personal policy today while you are happily employed, its waiting periods will quietly mature in the background. By the time you change jobs or retire, your personal shield is fully active and covers everything from Day 1.

2. Insurance is Bought with “Good Health,” Not Just Money 🩺

Company Health Insurance vs Personal Policy: Today you are young and healthy, which is why you feel secure under the corporate umbrella. But what if you develop a lifestyle illness like high blood pressure or thyroid issues over the next few years, and then lose or change your job? When you try to buy a personal health policy with those medical conditions, insurance companies might reject your application completely or charge a massive premium loading.

3. Rented House vs. Owning Your Home (The Ownership Problem) 🏢

Company Health Insurance vs Personal Policy: Company health insurance is like living in a luxury company-provided rented apartment—it’s fantastic while you work there. But would you leave your family’s ultimate safety at the mercy of a landlord who can ask you to vacate at any time? A personal insurance policy is a home you own. No matter what happens to your job, no one can strip away your healthcare shield.

4. The Retirement Blind Spot 👴

Company Health Insurance vs Personal Policy: When do you actually need medical insurance the most? After age 60, when the body ages and medical risks skyrocket. Ironically, your corporate cover drops to zero (0) the exact day you retire. Trying to find a comprehensive, affordable health insurance policy at age 60 is incredibly difficult, highly expensive, and involves brutal medical screenings.

5. Hidden Limits and “One-Size-Fits-All” 📋

Company Health Insurance vs Personal Policy: Corporate policies are designed for the masses, not your specific family dynamic. They often come with restrictive hidden clauses like:

- Room Rent Capping: You might only be eligible for a twin-sharing room. If you choose a private single room, a massive proportionate penalty is deducted from your entire hospital bill, which you must pay out of pocket.

- Co-payment Clauses: You may have to bear 20% to 30% of the bill yourself if you claim for dependent elderly parents.

💡 The Smart Strategy: The Budget-Friendly “Super Top-Up”

Company Health Insurance vs Personal Policy: If premium costs are holding you back, you don’t need to buy a massive, expensive separate policy right away! You can keep your corporate insurance as your primary cover and attach a Personal Super Top-Up Policy to it (e.g., with a 5 Lakh deductible).

Because your company policy covers the initial 5 Lakhs, the premium for this personal policy is incredibly low—costing just a few thousand rupees a year. However, it locks in your “insurability” today and starts ticking off your waiting periods immediately!

Conclusion:

Company Health Insurance vs Personal Policy: Corporate health insurance is an excellent bonus, but it should never be your primary line of defense. Build a permanent shield for your family today, before a medical report or a resignation letter leaves you exposed.

Disclaimer: I hold a Diploma in Naturopathy and am an AMFI-Registered Mutual Fund Distributor and Licensed Insurance Advisor. This content is authored based on my studies in holistic wellness and professional expertise. The information provided is for educational purposes only and should not be treated as a substitute for professional medical advice, diagnosis, or treatment. Always seek the advice of your physician or other qualified health provider with any questions you may have regarding a medical condition. Furthermore, mutual fund investments are subject to market risks; please read all scheme documents carefully before investing.

🙋♂️ FAQs (Company Health Insurance vs Personal Policy)

Q1. Can I convert (port) my corporate health insurance into a personal policy after leaving my job?

Ans: Yes, under IRDAI regulations, you have the right to port a corporate group health insurance policy into an individual or family floater policy with the same insurance company. However, you must initiate this process at least 45 days before your official resignation or last working day. The final premium and approval will depend entirely on the insurer’s underwriting guidelines and your current health status.

Q2. If my employer provides a ₹5 Lakh cover, what should be the ideal sum insured for my personal Super Top-Up policy?

Ans: Ideally, you should select a Super Top-Up policy with a ₹5 Lakh deductible (matching your company cover) and a sum insured of ₹25 Lakh to ₹50 Lakh. This effectively expands your total health shield to ₹25–50 Lakh. Because of the deductible, the premium for this backup policy remains exceptionally low and budget-friendly.

Q3. Will the time spent under corporate insurance waive the waiting periods in my new personal policy?

Ans: If you buy a separate, independent personal policy while working, its waiting periods run independently and mature over time in the background. However, if you are porting your corporate policy directly upon leaving, you may get continuous coverage benefits (credit for time served) for standard waiting periods, though the new personal policy’s premium will adjust based on your age and medical history.

Q4. Can I claim tax benefits under Section 80D for my corporate health insurance?

Ans: No, you cannot claim tax deductions under Section 80D for the health insurance premium that your company pays on your behalf. Tax benefits are only applicable if you pay the premium out of your own pocket from your personal bank account for an individual or family policy.